Multi-Year Compounding Activism

Why Pershing Square might be an assymetric play for the long-term

This year has been one of the best on record for the S&P 500, yet investors are finding themselves in a peculiar bind—chasing after those elusive, risk-adjusted opportunities that promise good returns without the gut-wrenching volatility.

Amidst this uncertainty, Pershing Square (LN:PSH) (LN:PSHD) (NA:PSH) stands out like a lighthouse in a storm. Since 2004, it's not just kept pace—it's set the pace, outperforming the market with a consistency that's hard to ignore. And here's the kicker: it's currently trading at a NAV discount significantly below its historical average, potentially offering a once-in-a-cycle opportunity.

What is Pershing Square?

Pershing Square Holdings, Ltd. (PSH) is an investment entity structured as a closed-end fund, with a mission to achieve substantial long-term growth in shareholder value through strategic investments in a select portfolio of large-cap companies. Established in Guernsey in 2012, PSH initially operated as an open-ended scheme before transitioning to a closed-end format in 2014, allowing for a stable share count and more focused investment strategy. Its shares have been tradable on Euronext Amsterdam since October 2014, and on the London Stock Exchange's Main Market since May 2017.

Under the stewardship of Pershing Square Capital Management, L.P., led by the renowned investor Bill Ackman, PSH focuses on a concentrated portfolio, typically containing between 8 to 12 significant holdings. These are primarily North American companies known for their liquidity and potential for stable, recurring cash flows. The Investment Manager, PSCM, adopts an active role, engaging deeply with these companies to drive operational and strategic improvements, aiming to unlock and enhance shareholder value over the long term.

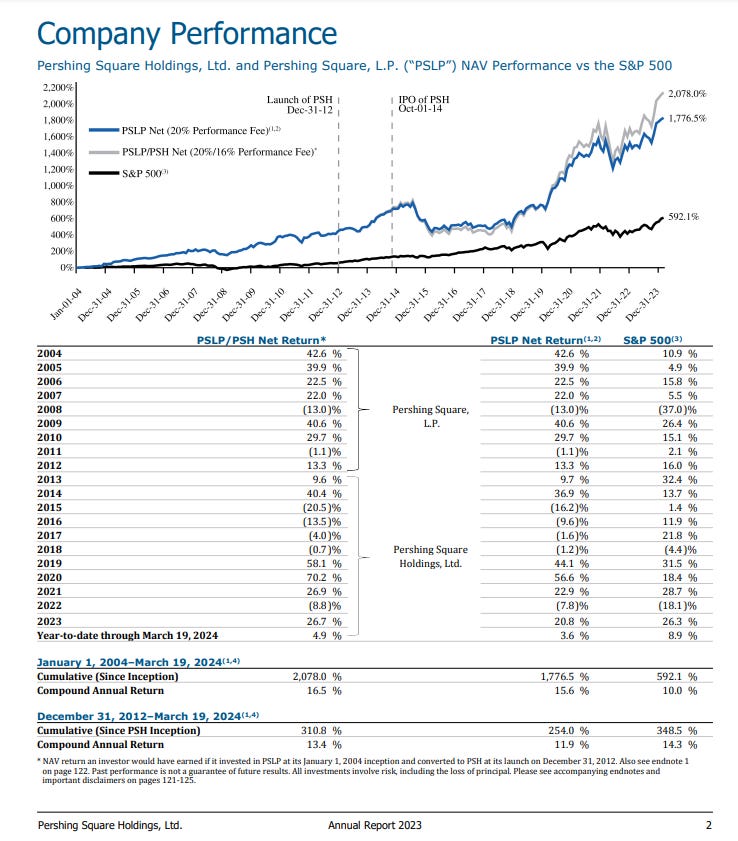

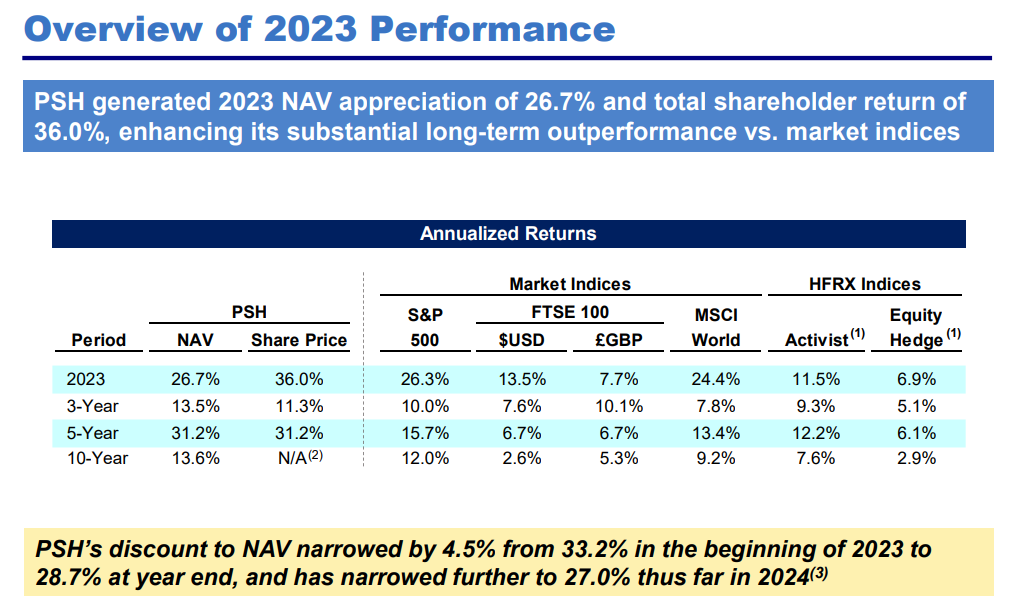

PSH's investment philosophy has proven effective, especially when there is a crisis period. The fund has been very effective to identify potential disasters, and benefitted from them which boasted an annualized net return of 15.7% over nearly two decades, significantly outpacing the S&P 500's average annual return of 10.1% for the same period. This has resulted in a cumulative net return of 1,932.7% for PSH, compared to the benchmark's 630.0%. To manage the inherent risks of such a concentrated investment approach, PSCM implements meticulous security selection, portfolio construction, and incorporates hedging strategies when advantageous, aiming to balance growth with risk management.

Pershing Square stands out in the investment world by managing its funds with what's known as permanent capital. Unlike many competitors who must cater to the demands of investors looking to withdraw their money annually, quarterly, monthly, or even daily, Pershing Square enjoys a stable capital base. This stability is a significant edge, allowing the firm to focus on long-term growth and seize opportunities during market downturns, times when others are pressured to sell off assets just to meet withdrawal requests. This permanent capital model not only provides the luxury of patience but also fosters strong, lasting partnerships with the management teams of the companies in which they invest. This has attracted some of the industry's top CEOs to join their portfolio companies.

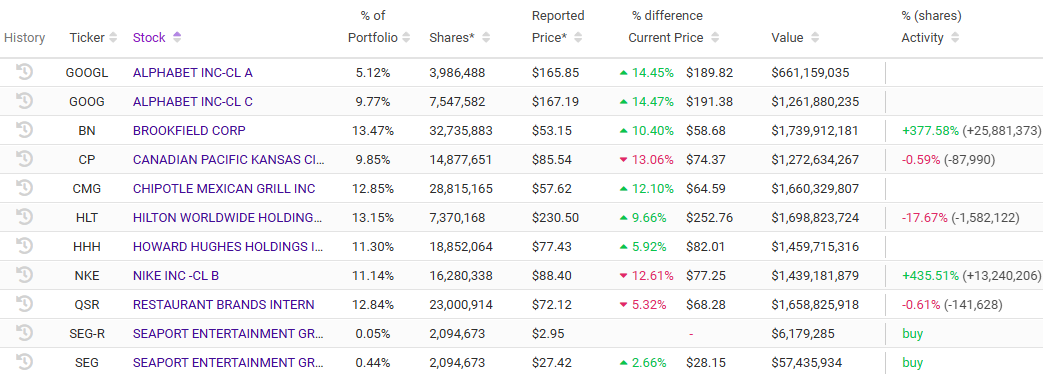

Pershing Square bases their investing approach in few key elements. They look for minimal capital dependent, undervalued cash cows that operates in an industry with strong barriers. It is similar to Berkshire style investing but include a lot more activism. They generally own a minority stake in the company and use their activism to push initiatives on majority shareholders that will unlock the value which will benefit the entire shareholders. Here is the 2024Q3 portfolio of the company:

The porfolio generally consist of a companies with a robust growth trajectory ahead with industry-leading sales. Some of the ownerships represent as low as 3% but another is (e.g. Howard Hughes Holdings) 38% ownership of the entire company. If you want to deep dive into the details of the reasoning behind the investment, you can look at their annual invester presentation to latest updates.

On the other hand, Pershing Square has a very popular portfolio manager: Bill Ackman who has 1.5 million followers on Twitter, who had took down the Harvard President for being unqualifed for the job and lastly threatened the Amsterdam exchange of delisting Pershing Square because of their stance against an attack Pro-Israeli soccer fans.

Contraversial Leader

Bill Ackman has become a figure of both intrigue and controversy in the financial world, known for his bold, often polarizing leadership that swings between genius and gamble. His audacious bets have indeed paid off enough times to cement his status as one of the world's most successful money managers. Over the last decade, his publicly listed Pershing Square Holdings (ISIN GG00BPFJTF46, UK:PSH) has seen its net asset value grow by an impressive 13.6% per annum, outstripping both the S&P 500's 12.6% and the FTSE-100's 5.3% annual returns. Ackman's journey in managing money, which started back in 1992, has not only showcased his ability to regularly outperform the markets but has also built his personal fortune to near USD 10 billion, largely through performance fees from his clients and his own successful investments.

One of Ackman's most talked-about gambles was his investment in what was then Valeant Pharmaceuticals, now Bausch Health (ISIN CA0717341071, CA:BHC). He championed Valeant's aggressive acquisition and cost-cutting strategy, which initially seemed like a masterstroke. However, the company's fall from grace due to accusations of unethical practices painted Ackman's loyalty as both a testament to his commitment and a blind spot in his leadership.

Equally dramatic was his short-selling campaign against Herbalife (ISIN KYG4412G1010, NYSE:HLF), where Ackman bet a billion dollars that the company was a pyramid scheme, leading to one of the most publicized financial battles in recent history. His relentless pursuit included public speeches, detailed research reports, and even a documentary, turning the confrontation into a spectacle. Despite not achieving the financial outcome he hoped for with Herbalife, this venture highlighted Ackman's fearless leadership style, where he's willing to take on giants with all the theatricality of a Wall Street drama.

Ackman's approach, characterized by his tenacity and a penchant for dramatic showdowns, has made him a figure both admired for his audacity and critiqued for his missteps. His leadership, while controversial, has undeniably left a significant imprint on the world of finance, showcasing a man who's as fearless in his investments as he is in his public battles. Here is the investor pitch that accused Herbalife as a scam, it is quite a funny one to read.

Ackman, on the other hand, unleashed his full support for Trump during the presidency campaign. His latest interview on CNBC has highlighted “Stepping into the most pro-growth, pro-business administration in my adult lifetime” As being a man with high influence, there is no doubt that the Ackman will be one step ahead than others, potentially pushing the regulations or deragulations that will create value for his shareholders, and also a fat fee for himself.

Why the Huge NAV Discount?

Perhaps the most attractive aspect of the stock is the huge NAV discount after the announcement about the U.S. Listing. Bill Ackman's Pershing Square Capital Management had high hopes when they decided to launch Pershing Square USA (PSUS), aiming for a U.S. listing to broaden their investor base. The primary goal was to access a significant amount of capital from American investors, with an initial fundraising target of a staggering $25 billion. Ackman, known for his bold investment strategies and outspoken nature on social media, saw this as an opportunity to leverage his brand to draw both retail and institutional investors into his unique closed-end fund structure. The idea was to simplify investment in Pershing Square's strategies, offering a vehicle with permanent capital that could execute long-term investments without the pressure of redemptions.

However, the journey to the IPO was fraught with challenges. The initial excitement quickly waned as the fund had to slash its fundraising goal to just $2 billion, signaling a considerable lack of investor enthusiasm or trust in the proposed structure at the planned valuation. Market volatility could have played a role, making investors cautious about committing to a new fund, especially one in a closed-end format known for occasionally trading at discounts to its net asset value (NAV). Moreover, there might have been concerns about the complexities of the CEF structure, including liquidity issues and the potential for the fund to trade at a discount, which could deter those looking for simpler investment vehicles.

Ultimately, the IPO was canceled due to a reevaluation based on investor feedback. Bill Ackman took to X (formerly Twitter) to announce the withdrawal, explaining the need to revisit the fund's structure to make it more appealing or straightforward for investors. This decision was likely influenced by the lukewarm reception during roadshows, suggesting that the market conditions or investor appetite at the time weren't conducive for the kind of reception Pershing Square had hoped for. During 2023, high hopes for the IPO has narrowed the NAV discount. Eventually, It has again widened by a big percentage to almost 30%, bigger than the historical averages of the fund.

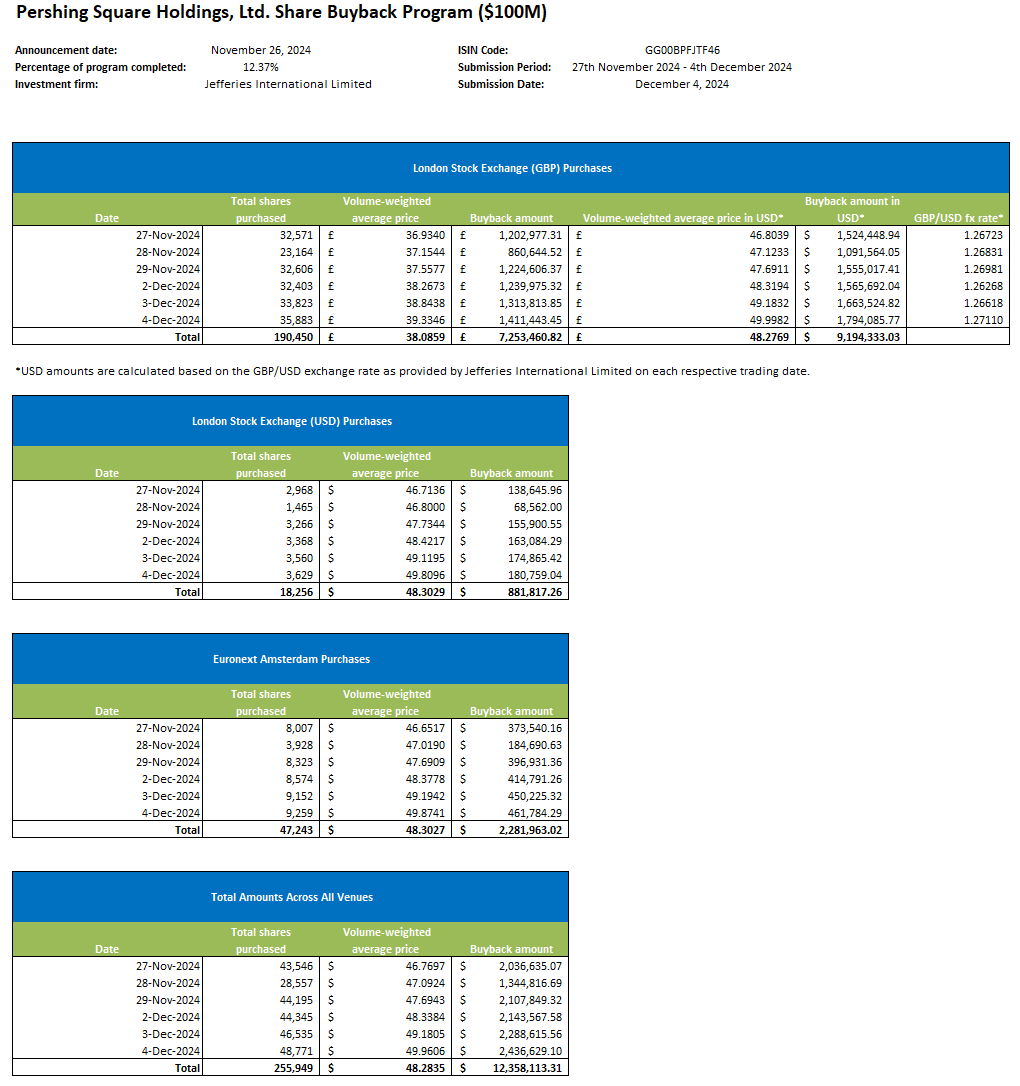

Additionally, the company has started a buyback program this year since the stock price fell by 18% after the IPO. The buyback program is relatively small, representing around 1% of the Market Cap. However, this signifies a potential belief that the share price is undervalued and it helps to return money to shareholders while limiting the downside.

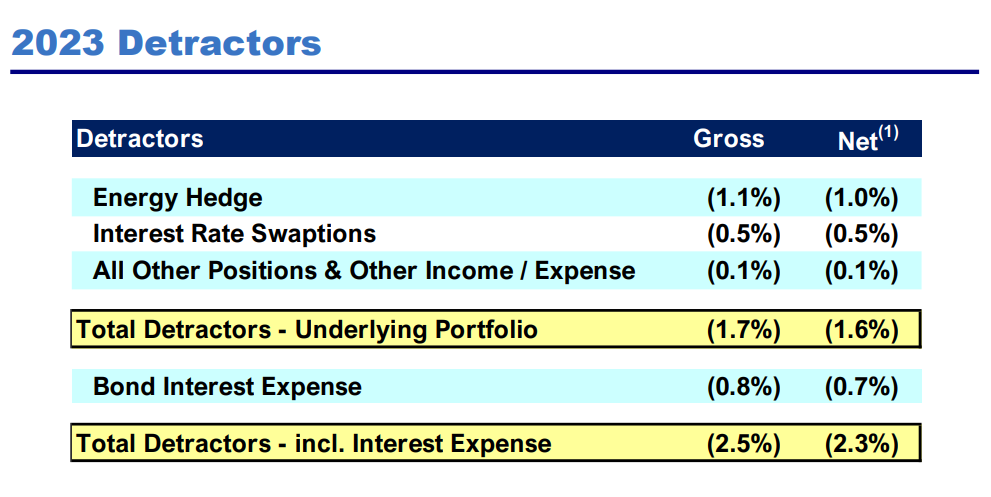

Investing in Pershing Square during an S&P boom under Trump's presidency might seem like trying to catch a falling knife, but let's slice through the numbers and see why it might just be the sharpest tool in the shed. The company was negatively affected by their hedges and interest rate swaps in 2023, which must have felt like they should during one of the best S&P performances. Currently, nearly 12% ($1.8 billion) of their assets are in cash and cash equivalents, just chilling, waiting for the right moment to pounce. This diversified basket of assets could cushion the fall or even bounce back higher if played smartly, kind of like a financial insurance. And let's face it, in the investment game, what's a few percentage points when you're playing chess with the market?

DISCLAIMER: The material published in this report is part of a website that is a personal blog. Neither the article nor the website is a regulated financial advisor in any jurisdiction